The key to financial freedom is to save money and invest it so that it grows passively over time. The more money you can save, the quicker you will be able to reach your goals.

I always knew this and understood that I needed to increase my savings in order to become wealthier. When my wife and I got married, it quickly became apparent that we needed to track our expenses closely to be able to save appropriately.

We were able to save more money every month by creating a monthly budget. A budget is one of the most powerful tools that you can use to improve your financial stability.

What is a Personal Budget?

A written personal budget is a way to track your income and expenses. It shows exactly where your money is going each month and if you actually are saving anything. By tracking your spending habits, you’ll better understand if there are areas you can cut back on.

At the base of it, a personal budget is a mathematical equation. Your monthly savings is equal to your income minus all of your expenses. If your savings turn out to be negative, you are actually over-spending and would have to dip into other money to pay those expenses.

Savings = Income – Fixed Expenses – Variable Expenses

A personal budget allows you to make sure that you are actually saving money each month. By getting more granular and understanding your expenses, you’ll be able to better understand if you are overspending in any one area.

Using a monthly frequency to track your budget makes the most sense because the majority of bills are on a monthly basis. It also lets you track changes frequently enough to make corrections if something starts to get out of whack.

I also recommend looking at your budget at the end of each year to see if you hit your larger goals. This will show how well you did over multiple months and help form your decisions for the next year. There are some bills that are paid on an annual or semi-annual basis, like taxes, so a yearly review of your budget will show those trends.

As an example, here is our 2020 year-end budget summary.

Download Budget Tracking Spreadsheet

How to Track Your Budget

The first step towards creating your budget is to use one central place that you can record your income and expenses. An Excel spreadsheet is a great way to start to do this because it can be created quickly and adjusted to meet your needs.

Just list all of your income sources and fixed and variable expenses for the month. A few quick calculations will give you how much you are saving and what percentage that is.

Feel free to use our own budget spreadsheet to get started even faster. Download a copy of our budget tracker spreadsheet when you join our free membership. We also have a list of free budget spreadsheet templates that you can use.

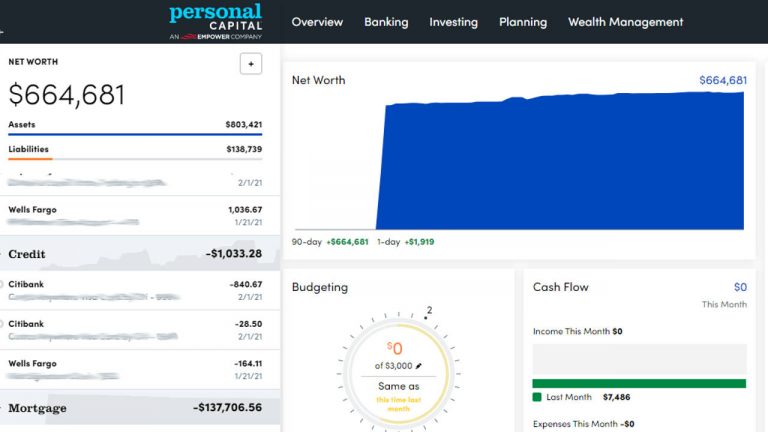

Another option is to use an app like Personal Capital to track your budget automatically for you. I signed up with Personal Capital a few months ago and am in love with how powerful it is.

Related: Read our full review of the Personal Capital app

By syncing your bank accounts with the app, it is able to track all your expenses, investments, and income in real time to calculate your net worth and monthly budget.

Collect Your Financial Statements

Once you have a method of tracking your budget in once place, you need to start collecting the data to fill it out. Make a list of every financial account you have, along with any assets you may own. Hopefully, you have access to everything through online portals, otherwise you’ll need to gather the paper statements.

Include your bank accounts, both checking and savings. If you make purchases through a credit card, include that so you know specifically what your expenses break down as. Don’t forget to include your monthly mortgage or rent payment so you can build a full picture of expenses.

Determine Your Monthly Income

The first step to creating your monthly budget is to determine your take-home income. This is important to calculate after taxes and contributions to your retirement accounts so that you know the max that you can spend in a month.

The easiest way I do this is by looking at my bank statement to see exactly what has been deposited from my company for the month. I do contribute to my retirement account, but that doesn’t need to be included in your budget calculation. However, that information is important if you are trying to determine your net worth.

Don’t forget to include any other income you might get beside your main job. If you have side hustles that make money, include that income in your tracker.

Record All Your Fixed Expenses

Now that you’ve determined how much money has flowed into your bank account, lets figure out how much has gone out. There are two types of expenses that you will have, fixed and variable.

Fixed expenses are the ones that remain the same every month. While some may fluctuate a little over time, these are the most common fixed expenses:

- Mortgage or rent

- Utilities – heating, electric, water

- Cell phone

- Phone, internet, cable

- Groceries

- Car payments

- Loan payments

- Taxes

Write down all of these costs for each month to get a good sense of what your base spending level is.

Add Your Variable Expenses

The next piece to add are your variable, or discretionary, spending for the month. These are the expenses that will change every month and may not consistently show up in your budget.

Variable expenses can include:

- Eating out at restaurants

- Entertainment

- Vacations

- A new game, toy, or shiny object

- Gifts

As you’ll notice, these are the items that could be considered as “extra” and not required strictly for survival. They are the expenses that make life fun and happy.

The difference is that, at a minimum, you need to go to the grocery store and buy X amount of money per month to eat. However, eating out at restaurants and getting take-out is more expensive and is generally done to help simplify your life and for the entertainment.

Total Your Income and Expenses for the Month

Now that you have your data recorded in one place, it’s time to add everything up. If you’re using a spreadsheet, you should have one section that has your total income for the month. Take that and subtract the total expenses that you spent money on for the month.

Hopefully, the number you get is positive. This means that you have some money left over after your expenses to save or invest. If your number is negative, you actually spent more money during that month than you earned.

Do this every month for a year to see how your budget trends. In my own budget, I may have one month where my expenses are higher than income but the rest of the months I save considerably.

But why would I “over-spend” for a month? Vacation! If we go on a larger vacation and pay for the bulk of it in one month, it will look like I have a huge expense. In reality, I have been saving for the previous 6 months and are prepared for this larger cost. Having one or two high-expense months is perfectly fine as long as you have an annual budget and a plan to pay for those costs.

TIP: Automate Your Budgeting

There is an easier way to track your monthly expenses than using spreadsheets and logging into each of your bank accounts. My number one recommendation is to automate tracking your expenses, savings, and net worth by using Personal Capital.

Sign up up for a free Personal Capital account to get started.

How Much Should I Be Saving?

The amount you save will vary significantly based on several factors, including how much you make, your cost of living, and how much you value your entertainment. It also depends on your short and long-term financial goals. Having a personal budget will allow you to see the breakdown of what you are spending money on and adjust for those goals.

In general, many advisers will say that 50% of your income should go to your fixed expenses like rent, food, and utilities. 20% should go towards your savings in order to build an emergency fund and your overall wealth. The final 30% can then be used for your variable discretionary spending.

I highly recommend paying your bills in that order. Your fixed expenses come first because they are required for a stable, debt-free life. After that, always pay yourself first by moving money to a dedicated savings account or investment portfolio.

If you have money left over, then you can either spend it on entertainment or continue to save even more.

Personally, I have reduced my expenses as much as possible and am able to save around 45% of my monthly income every month. We still go out and have fun, but our priority is saving and investing right now. That money get reinvested monthly into our mortgage or investment accounts.

How to Save Money with a Personal Budget

Saving money starts with understanding where your money goes. The only two ways to save more is to either make more money or reduce your expenses.

While we all want to make more money, finding extra income can take time and be harder for some people. The easiest way to start saving more money is to find places to reduce your expenses.

Look at your monthly budget after a few months to see if the numbers make sense. Are you paying for three different subscription services for TV and movies? Save money by choosing one and getting rid of the others.

How about eating out? If you tend to eat out or get prepared food multiple times per week, think about reducing that number to once a week. Enjoy that date night with your partner but just reduce the frequency a little bit.

Rent or mortgage payments are generally the largest fixed expense people have. If you’re serious about saving more money, you may want to think about finding more affordable housing or renting out a spare room.

Saving money comes at a cost. You’ll need to change your priorities and make compromises in the short term to save more money. It’s not easy for everyone, but is well worth it once you start to see progress towards your financial goals.

Subscribe to our exclusive Couple Wealth membership for free and download our budget tracking spreadsheet.