2020 was the first year that I really started to take our finance seriously. I started to do more research into investments and to think about what we should do with our money. While the rest of the year was pretty terrible with COVID-19 and murder hornets, we had a solid year financially.

That all started by being able to track and trend our finances. From there, we adjusted our goals and came up with a strategy to meet them.

The first thing I did was to create a simple spreadsheet that tracked the balances of all our accounts. I included each of our bank accounts, investments, and retirement accounts to give a full picture of where we stand. Every month, I would login to each account and record the balance at that time.

Sign up for free to download to my net worth spreadsheet and get exclusive financial planning tips.

By doing so, I was able to calculate our net worth and how well our investments were performing. Net worth is calculated as the the sum of all assets minus any debt or liabilities. For example, you may have $100,000 in your bank and retirement accounts. If you have a $20,000 car loan outstanding, your net worth would be $80,000.

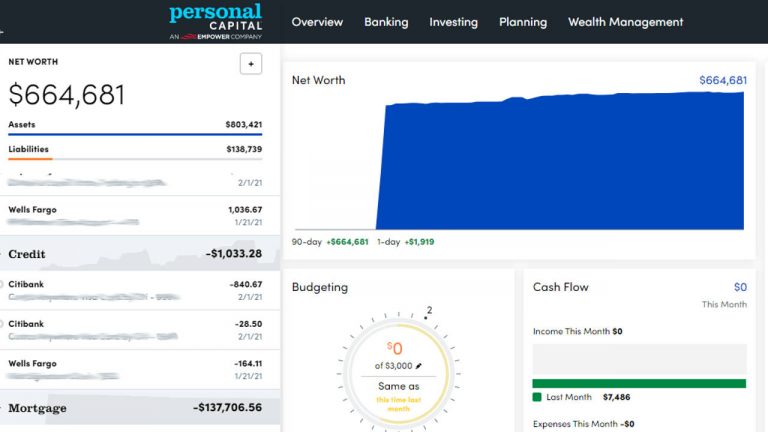

A couple months ago, I signed up for Personal Capital and it is an absolute game-changer. It is a free app that automatically tracks all of your financial accounts, helping you manage your budget, savings, and net worth. I highly recommend checking it out if you are serious about building your wealth.

2020 Financial Goals

Going into 2020, we had some basic financial goals. We wanted to pay down our mortgage as much as possible while also increasing our investments. We also wanted to make sure we still had enough cash in our emergency fund after building it in 2019.

I will say that our financial goals are based around our strategy being a little more conservative than some people. Never being much of a gambler, I’d much rather have a solid, medium performing portfolio than a very risky strategy. This means that many of our goals are based around building a solid financial base first. Once we have that, we can branch out into higher-performing investments later.

Taking on more risk in our investment strategy would certainly allow us to make more money long-term. It also opens up the possibility of losing more if there was a recession or something else unexpected happens. 2020 was a tough year with COVID-19 disrupting the markets, an election, and an expected recession. Since we wanted to provide a solid base for our family, we have been more conservative this past year.

Of course, you should determine your comfort level while investing, and then create your own strategy.

Here are the list of our goals for the year:

Maintain an Emergency Fund for at Least 6 Months

We wanted to make sure that we are able to survive at least 6 months if both of us lost our jobs or had a medical emergency. While we hope to never use it, it gives us a sense of security to have liquid assets for emergencies.

Going into 2020, we had already built our emergency fund, so there wasn’t anything else we needed to do this year. We left our 6 months of savings in a high-yield savings account to help minimize losing value to inflation. In the beginning of the year, we were earning an interest rate of 1.85%, but that has since dropped to 0.60%.

Maintain Cash Reserves

As a family, we know that we may need some cash in the next couple of years for larger investments. We are starting to plan for babies and know that there is a good chance we will need to purchase new cars soon. We are stretching our cars as long as possible but, with our luck, we’ll probably have them both die at once. On top of that, we’d like to have enough cash to be able to do some travel and home improvements without worrying about them.

That means that we need to have enough cash set aside that is liquid and easy to get to. We didn’t want to tie it up in the stock market or other investments that could be harder to get to quickly. Instead, we put the money into another high-yield saving account to earn a little interest while being easy to get to.

Like our emergency fund, we had built our cash savings to a point where we felt comfortable going into 2020. The goal of this year was to maintain that level and replenish our cash if any was used for expenses.

Contribute to Our Retirement Accounts

Both of our jobs have attractive retirement programs and provide 401k’s with matches. Jane and I both are contributing 13% of our salaries to our 401k‘s and have a 3% match. Having consistently contributed 15% or more every year since we started working, we now have a sizeable chunk invested in our retirement accounts.

The goal for 2020 was to continue to contribute the same amount and make sure we get the full company match. We also took a look at our asset allocation and made a few changes to make sure it was in line with our investment strategy. For example, we adjusted it to slightly increase the amount of bonds to make it a little more conservative.

Maximize Our House Equity

Our most significant goal for 2020 was to pay down the house mortgage as much as we could while also hitting our other goals. We decided to do this for two reasons.

- It would allow us a great deal of financial freedom if we pay off the mortgage. We would have no debt and would not need to worry about paying a monthly payment. Since our mortgage is our single biggest expense, eliminating it would give us greater freedom to do other things. Also, it opens up the possibility of not needing us both to work and being able to live on a smaller income.

- With the stock market looking pretty turbulent through COVID and the election, many experts thought that a stock market recession was likely. To us, investments in 2020 were not guaranteed and may likely not go up very much. In contrast, we knew that paying down our mortgage was a guaranteed 4.25% return.

This meant that we put the majority of our extra savings towards the house. We paid every two weeks and would round up significantly. While I would pay the actual mortgage due plus about $1700 extra each month, Jane would also contribute $2,000 to $3,000.

When we got our tax refund, we put that towards the house. We had pre-paid a few baseball game tickets that were canceled due to COVID, so we put that money towards the house.

At the time of writing, we are exactly 50% through our mortgage. Since the interest payments are about half what they were the first year, we are seeing much better progress now.

Put Everything Else Into Investments

Our final goal for 2020 was to put any remaining savings into investments including REITs, stocks, and bonds. While paying the mortgage was a major goal, we also want to create passive income through investing. To do that, we need to put our cash regularly into diversified investments that we plan to hold for at least 5 years. This is important to note, since we are ok with not touching that money in the short term.

Our two main investment platforms of choice are Fundrise and M1 Finance. Fundrise allows us to invest in real estate and has returned around 4% this year. In other good years, it has performed much better, at around 8% to 11%. We chose Fundrise as a way to diversify out of the stock market and hopefully provide more stable dividend income.

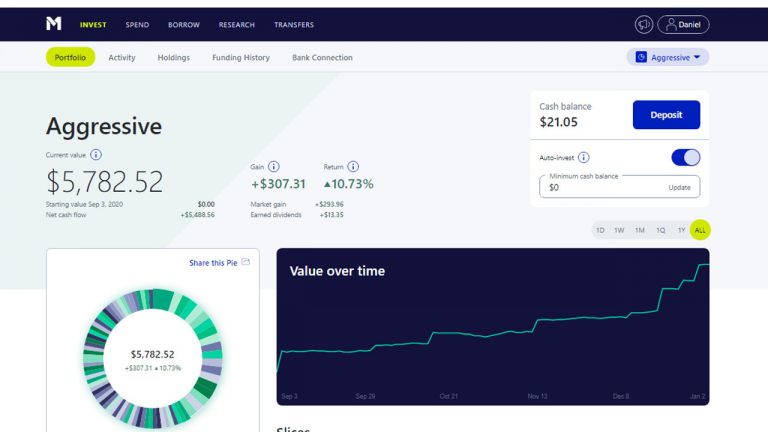

We also use M1 Finance to create “pies” of stocks and bonds. This allows us to create our own investment strategy and determine exactly which stocks we want to invest in. As of right now, we have a conservative pie that proved to do very well throughout the COVID recession and is currently up 9.18%. We also have a more aggressive pie that has growth stocks and high-yield dividend stocks.

COVID-19 Impact in 2020

Most of the year was overshadowed by the COVID-19 pandemic that swept the world. I don’t think we can talk about 2020 without acknowledging the impact this pandemic created.

While millions of people lost their jobs and were laid off, my wife and I were fortunate enough to remain employed. I cannot be more thankful to be financially stable and not have to worry about paying bills. The COVID recession is a great reminder of why we all need enough emergency savings to get us through hard times.

The pandemic forced us to cancel our travel plans and stay home this year. We sadly got our money back for a European cruise, several concerts, and sports games that we had pre-ordered. Suddenly, we had a ton of extra money back in our bank account that we had planned on spending.

We took that money and put it work paying down our mortgage and investing it. We still treated ourselves to a few small things, but the majority of that money went back into our net worth.

All in all, we were lucky to have stable salaries and a solid emergency savings to help us weather the COVID-19 recession. We were actually able to save more money than normal by staying in and this helped us reach our financial goals.

Getting Ready for 2021

Overall, we met our goals for 2020 and feel comfortable with were we got to in the past year. Our net worth crossed $500,000 and has continued to go up every month. And, we have learned a lot about what will help us achieve financial freedom as a couple.

Here is an approximate breakdown of our net worth to see how we are currently allocated.

While we still have another month in this year, it is a good time to start thinking about our goals for 2021. I expect that we will continue to grow our investment and home equity percentages over the next year. Our cash and emergency fund will stay approximately the same in value, so their percentage should decrease as overall net worth increases.

2020 brought a unique set of challenges to the entire world but I am grateful to be in a position where our family could continue to grow financially.

What about you? Do you have specific goals and did you reach them for the year?